Financial Markets 25/11/2025

The beacon of the markets:

The resurgence of the two main market fears, high valuations in the technology sector and the billions being invested in AI development, together with doubts about the Fed’s next move, caused corrections of some magnitude in the main stock markets, despite the emergence of new information/rumours that could alter the future of the stock markets. On the one hand, the possible negotiation of a peace agreement in Ukraine, with some pressure from the United States for Kiev to give in, could give the stock markets a boost again, a circumstance that could also occur in Japan with the approval of a financial stimulus package equivalent to 3.2% of the country’s GDP, without overlooking the resurgence of news that China could implement an incentive plan aimed at boosting both domestic demand and the recovery of its property market. On the other hand, news regarding the US economy continues to be quite positive, as was the case with job creation in September and the current estimate of GDP for Q4 2025 by the Atlanta Fed, which puts it at 4.2%, data that would not facilitate the Fed’s decision to lower rates at its meeting on 10 December.

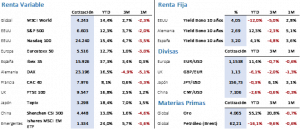

What seems clear is that, following the sharp rebound in the markets from their April lows, investors need much greater visibility on the global economic outlook before continuing with their purchases. Not even Nvidia was able to turn the situation around; its once again extraordinary results and forecasts for the coming months only allowed for a fleeting recovery in the technology indices that lasted less than 24 hours. Thus, at the end of the week, the S&P 500 was down 1.95% to close at 6,602.99 points, while the Nasdaq 100 closed at 24,239.57, down 2.71% from the previous week. In Europe, the situation was very similar. After reaching new all-time highs the previous week, this week saw declines of more than 3%, with the Euro Stoxx closing at 5,523.20 points and the Ibex 35 at 15,830.80.

In the European debt market, changes in yields were minimal. The Bund fell 2 bps to 2.70%, while the 10-year bond remained stable at 3.22%. The United States followed the same path with the 10-year Treasury, but on Friday everything changed and the week ended with a fall of 9 bps to 4.06%. Throughout the week, the market was pricing in a probability of around 30% that the Fed would cut rates in December, i.e. the market did not believe that such a cut would occur, but the rise in the unemployment rate to 4.4% and a notable decline in inflation expectations in the polls raised that probability back to 69%. If there is a cut, both the technology sector and small companies will benefit, which led to a recovery from Friday’s session lows.

The increased volatility seen in the markets, a sign of uncertainty, has not carried over to safe-haven assets in 2025. Instead of rising sharply, gold fell 0.36% during the week to close at USD 4,079.50/ounce, but as in previous weeks, silver was the metal that experienced the greatest price volatility during the week, with a 9% swing between its high and low. The notable cumulative rises in the precious metals sector are driving these larger movements, but the consensus among experts remains that, although there may be significant corrections in the short term, the market still has room for growth in the long term. Brent crude corrected by 2.84% to close at USD 62.56/bbl. On the one hand, the potential ceasefire in Ukraine would free up Russian crude oil on the market, i.e. greater supply pressure, and on the other hand, the appreciation of the USD favours a fall in prices.

In terms of macroeconomics, beyond the data discussed above, we would highlight, on the one hand, that inflation in Europe has been confirmed at 2.1% according to the CPI, and on the other, that the provisional PMI data for November show the same trend on both sides of the Atlantic, with the manufacturing sector slightly below forecasts while the services sector has improved, with the aggregate figure exceeding estimates. Throughout this week, we will learn about various data on the US economy, but much of it is already old, such as the PCE for September, and the second revision of the GDP data for the third quarter of 2025, which initially stood at 3.8%, will be published. More than 94% of companies have already reported their results for the season, with very positive results. 83% have surprised on the upside, compared to only 13% that have disappointed, generating earnings per share growth of 14.7% compared to the initial forecast of 8.5%.

The quote:

And we leave you with the following quote from Christian Lous Lange, Norwegian historian, pacifist and Nobel Peace Prize winner: ‘Within every social group there is a prevailing sense of solidarity, an urgent need to work together and enjoy doing so, which represents a high moral value.’

Summary of the performance of major financial assets (24/11/2025)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.