Financial Markets 21/04/2026

The Beacon of the Markets:

Against a relatively positive backdrop for financial markets, and despite widespread doubts about the ceasefire, Iran surprised everyone on Friday afternoon by announcing it was authorizing the free passage of ships through the Strait of Hormuz. This was one of the essential conditions imposed by the United States for reaching a definitive ceasefire agreement, along with a commitment not to develop nuclear weapons. The reaction was immediate, with significant buying across various asset classes, with the exception of oil, which fell by nearly 10% on Friday. The interpretation of the Iranian message, as is often the case, was overly zealous, and by the close of trading, bond, equity, and commodity markets were all below their session highs.

The positive environment for investors could continue, but we must remember that the 14-day truce ends on April 22. The betting odds suggest an extension of the trade war could be announced given Iran’s latest move, and while there’s no certainty this will happen, the reality is that US indices have once again reached all-time highs, and therefore, we’ll likely hear repeatedly that valuations are fair again. Consequently, any corrections that occur could be significant, especially considering the war isn’t over and the current market valuation might encourage a systematic reduction of risk and a wait-and-see approach with a more conservative portfolio position. However, as we’ve seen recently, markets don’t give warnings and react very quickly, and staying out is often a risky option, to say the least.

The negative bias was seen in the macroeconomy. Several indicators made it clear that, after seven weeks of the Strait of Hormuz closure, the effects are beginning to be felt in the real economy. In China, two key data points stand out: first, the unemployment rate rose, contrary to market expectations; and second, exports declined sharply, increasing by 2.5% in March compared to the expected 11% and the 22% growth in the previous month. In Europe, final inflation for March rose to 2.6% from 1.9% in February. Finally, in the United States, the industrial production index for March fell by 0.5%, compared to the anticipated 0.1% growth. However, on the other hand, markets have once again focused more attention on corporate earnings, which, with exceptions such as Netflix, continue to be very positive, both in terms of the figures reported for the first quarter and the guidance provided for the coming quarters.

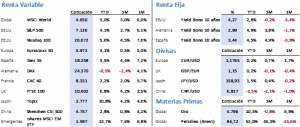

For the third consecutive week, stock markets experienced widespread gains, which were particularly notable in the United States. Thus, the S&P 500 rose 4.24% to close at 7,106.26 points, after reaching all-time highs on Thursday and Friday. The Nasdaq 100 was one of the biggest beneficiaries of the renewed optimism, finishing 6.20% higher at 26,672.43 points. The new geopolitical landscape is expected to reduce the likelihood of interest rate hikes, and under this premise, the technology sector is one of the sectors that stands to benefit. In Europe, the gains were significantly lower, probably due to the time the European market closed. The Euro Stoxx 50 finished at 6,057.71 points, posting a gain of 2.22%, and the IBEX 35 closed at 18,484.50 points, or 1.54%. European indices did not reach all-time highs, but came very close.

As for the bond market, the trend was the same: buying the asset in response to easing global tensions, as long-term yields remain attractive. The 10-year Treasury closed with a yield of 4.24%, a correction of 8 basis points for the week, the same as the Bund, which closed at 2.97%, breaking the psychological barrier of 3%. Meanwhile, the Bond yield fell 12 basis points for the week, ending with a yield of 3.39%. In any case, the main difference between equities and fixed income is that, while the former have already recovered all the ground lost since the previous yearly highs, the latter are still halfway between their 2026 high and low. The final impact on inflation and its repercussions on interest rates will not be known for several quarters.

Regarding alternative markets, the most notable event was the drop in oil prices on Friday, which fell by nearly 10%, leaving the weekly closing price at $90.38/bbl, representing a decline of over 5% for the week. Gold rose 1.93% to $4,879.60/oz, buoyed by new interest rate and inflation forecasts. Finally, the devaluation of the USD against the euro was significant; it closed at 1.1764, down 0.38%, but had fallen by nearly 2% during the week, approaching the 1.19 level.

After one week since the start of earnings season, we highlight the strong corporate performance seen so far. Forty-eight companies have already reported their results, reflecting EPS growth of 14.4%, very much in line with the 14.1% we saw in the fourth quarter of 2025.

The quote: And we leave you with this quote from Leo Tolstoy, the Russian writer considered one of the most important figures in world literature: “Ambition is not well-suited to kindness, but rather to pride, cunning, and cruelty.”

Summary of the performance of key financial assets (April 20, 2026)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.