Financial Markets 05/05/2026

With the fourth month of the year concluded and the second month of conflict in Iran, financial markets are maintaining the tone observed in recent weeks. Stock markets have once again reached new highs, driven mainly by the technology sector, which continues to be supported by very solid corporate earnings. By contrast, the tension stemming from the conflict in Iran —in a phase of formal truce, but with a high level of rhetorical confrontation between the parties— is being reflected more intensely in the commodities and debt markets. The closure of the Strait of Hormuz keeps oil prices at levels significantly higher than those considered reasonable, reinforcing expectations of high inflation in 2026 and, consequently, an interest rate environment with an upward bias.

During the week, the main central banks met expectations, and both the ECB and the Fed kept interest rates unchanged. In their subsequent statements, both warned of the potential deterioration in economic growth resulting from the rise in inflation, which in just two months has increased by more than 1% and is likely to eventually take its toll on the major economies. In Europe, the ECB’s tone was more explicit in anticipating a possible 25 basis point rate hike at the June meeting if price developments do not show substantial improvement.

On the macroeconomic front, the first effects of the inflationary environment are beginning to be observed in key indicators. PMI indices continue to reflect a high degree of pessimism, especially in the services sector. In Europe, the preliminary April CPI stood at 3%, compared to 2.6% in March and 1.9% in February, reinforcing concerns about the persistence of inflationary pressures. In addition, GDP growth slowed more than expected to +0.8%. In the United States, first-quarter GDP growth also fell short of estimates, although it remains at a healthy level after rising by 2%. Meanwhile, March PCE rose to 3.5%, once again moving away from the official 2% target. Despite this, the labor market continues to show surprising strength, with weekly jobless claims at multi-year lows.

Looking ahead to the current week, the main focus will be on the release of the final April PMIs and retail sales data in Europe. In the United States, in addition to the PMIs, the market will pay close attention to labor market figures, particularly the unemployment rate and nonfarm payrolls, which will be released on Friday.

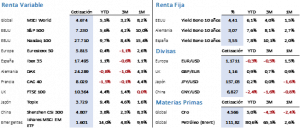

The main stock exchanges closed the week with moderate gains, supported by the strength of corporate earnings and particularly positive guidance. Notably, both the technology sector and small-cap companies performed well, showing remarkable strength in a rising interest rate environment that has historically been adverse for this type of company. The S&P 500 rose by 0.91% to 7,230.12 points, marking its tenth annual high. The Nasdaq 100 increased by 1.49% to 27,710.36 points, despite Meta’s weekly drop of over 9% after reporting strong results but revising its spending guidance upward for the fiscal year. In Europe, the Euro Stoxx 50 remained virtually unchanged, closing at 5,881.51 points, while the Ibex 35 rose by 0.49% to 17,781 points.

Fixed income once again acted as the main barometer of risk aversion. Elevated geopolitical tension in Iran, together with rising inflation expectations and the risk of a resumption of the conflict, triggered outflows from more conservative assets and a broad increase in yields. The U.S. 10-year Treasury ended the week at 4.38%, seven basis points higher than the previous Friday. In Europe, the German Bund increased its yield by two basis points to 3.03%, while the Spanish bond rose by five basis points to 3.50%, although all of them closed well below their weekly highs.

In commodities markets, Brent oil once again drew attention, surpassing 126 USD per barrel during the week before ultimately closing at 108.17 USD, representing a weekly increase of 2.70%. Gold, weighed down by rising interest rates, fell by 2.69% to 4,661.4 USD per ounce, although it remained clearly above the week’s lows. The dollar, with lower volatility than in previous weeks against the euro, closed virtually unchanged at 1.1721.

The earnings season continues to confirm a very positive overall performance. As of last Friday, 63% of S&P 500 companies had reported their results, of which 84% exceeded estimates. Earnings per share growth currently stands at 27.1%, well above the initial forecast of 13.1%, with the technology sector being the main driver of this improvement.

The quote:

And we close with the following quote from Liam Neeson, a British-Irish actor naturalized as an American citizen: “When you help someone, do so with gratitude, for life has placed you in the position of the giver and not in the position of the one who needs help.”