Financial Markets 26/05/2026

Market Highlights:

The situation in the Middle East remained unchanged throughout the week, allowing investors to continue favoring risk assets. In this context, bond markets saw relative calm in recent sessions, which positively impacted portfolio valuations.

Furthermore, President Trump announced the cancellation of his weekend plans—coinciding with his son’s wedding—to remain at the White House in anticipation of potential events of paramount national importance. Since Sunday, reports have indicated that a final agreement with Iran could be imminent. Several members of the administration conveyed a very positive message in this regard, which, as has happened on previous occasions, was subsequently denied or downplayed by Iranian authorities.

On the economic front, the macroeconomic data released reaffirmed the divergences between the various economic blocs. In China, the unemployment rate improved, although industrial production fell more than expected, maintaining a similar dynamic to that observed in the last two years. Meanwhile, in Europe, the CPI rose to 3%, while the PMIs fell short of expectations, reflecting a still-weak economy, partly due to Brent crude oil prices above $100. In the United States, however, the economy continues to show strength, seemingly unaffected by the conflict in the Middle East. The PMIs remained at solid levels, particularly in the manufacturing sector. Furthermore, the GDP growth forecast for the current quarter was revised upward to 4.3%, and the weekly employment data remains robust. On the other hand, the Federal Reserve is signaling to the market that the next move will be an interest rate hike, a scenario anticipated by the market for December.

This week will be virtually devoid of macroeconomic data, with the United States being the main focus of attention. The first revision of GDP for the first quarter of 2026 (provisional figure of 2%) and the PCE for April will be published, with figures expected to be very similar to those observed in the CPI for the same month.

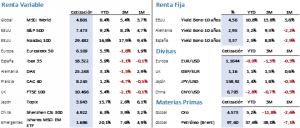

The positive tone was maintained in equity markets, reflected in the S&P 500’s eighth consecutive week of gains, a situation that has only occurred 20 times in the last 80 years. In Europe, the gains were somewhat stronger than in the rest of the world, reacting to the weaker performance seen in previous weeks, particularly affected by data pointing to an economic slowdown. Thus, the week ended with a 0.88% increase for the S&P 500, which closed at 7,473.47 points, very close to its all-time high. The Nasdaq 100 finished at 29,481.64 points, representing a weekly gain of 1.22%. The Euro Stoxx 50 rose 3.29% to 6,019.45 points, while the Ibex 35 gained 2.06%, closing at 17,985.30 points. The MSCI World, the global market benchmark, advanced 1.25% to 4,801.11 points at Friday’s close.

The bond market experienced an initial week of rising yields, which pushed several key benchmarks to levels not seen this year. However, a significant correction occurred on Thursday and Friday amid concerns about a potential agreement to end the conflict in Iran. The 10-year Treasury yield fell 3 basis points to 4.57%, after reaching a weekly high of 4.67%. In Europe, corrections reached 11 basis points for the Bund and 14 basis points for the Spanish bond, which closed at 3.04% and 3.47%, respectively. In any case, these yields remain between 30 and 50 basis points above their yearly lows, and current inflation forecasts for 2026 limit the possibility of further declines to those levels.

As for commodities, gold stood out, falling 0.85% to close at $4,523/oz despite the drop in bond yields. Silver, on the other hand, recovered some of the ground lost the previous week. Brent crude, which traded within a spread of over 10% during the week, fell 5.53% to close at $103.54/barrel, having traded below $100 and above $112. The high level of uncertainty continues to cause significant volatility, with this asset being the main reflection of current risk.

In the foreign exchange market, the week was marked by moderate movements, with a slight appreciation of the dollar against the euro of 0.21%, placing the exchange rate at 1.1603. The earnings season is nearing its end and continues to be very positive. More than 90% of companies have reported results, with 84% exceeding expectations. Average earnings per share growth stands at 26%, compared to the 13.1% expected at the start of the season, suggesting we will close out the best quarter in terms of results since 2021. Notably, Nvidia reported results above analysts’ forecasts. However, the strong gains accumulated in recent weeks have limited share price performance, although the correction observed so far remains contained.

Quote:

And we leave you with the following quote from Clinton «Clint» Eastwood Jr., American actor, director, screenwriter, and film producer: “I don’t believe in pessimism. If something isn’t working out, keep moving forward. If you think it’s going to rain, it will.”

Summary of the performance of major financial assets (May 25, 2026)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.