Financial Markets 23/06/2026

On June 20, a ceasefire agreement was reached between Iran and the United States, an event that was positively received by financial markets. However, the signing of the agreement has not resulted in a complete normalization of the geopolitical environment. Ongoing Israeli attacks in Lebanon continue to generate uncertainty, particularly in energy markets, where the supply of liquefied natural gas (LNG) and oil from the Persian Gulf remains under close scrutiny. In addition, Iran has postponed the meetings scheduled to advance toward a lasting peace agreement, arguing that Israeli military actions in third-party territories contradict the spirit of the commitments reached. Ultimately, although diplomatic progress has been made on paper, the situation in the Strait of Hormuz—one of the main sources of global tension in recent months—still shows no definitive resolution.

Meanwhile, market attention has shifted to the United States. The new Federal Reserve Chairman, Kevin Warsh, surprised investors with a distinctly hawkish speech following the FOMC meeting. The reaction was immediate: markets began pricing in up to two additional 25-basis-point rate hikes before year-end, and even a first move at the next meeting cannot be ruled out if the labor market remains strong and inflation continues to prove persistent. As a result, expectations of a more accommodative monetary policy and a weaker dollar quickly faded into the background, reigniting the debate over U.S. fiscal sustainability and its implications for investors.

In this context, the main conclusion is that volatility will remain present in the markets, although probably within more contained ranges. This will not prevent episodes of significant movements, both upward and downward, in an environment that will continue to be shaped by developments in geopolitics and monetary policy.

On the macroeconomic front, data continue to reflect a resilient global economy, in line with the messages delivered last week by the presidents of the Federal Reserve and the Bank of England. In China, industrial production showed a partial recovery, while the unemployment rate fell by one tenth to 5.1%. In Europe, inflation was confirmed at 3.2% in May, while investor confidence recorded a significant improvement. In the United States, although industrial production growth was moderate, both retail sales and the Philadelphia Fed manufacturing index exceeded consensus expectations. Looking ahead to this week, the macroeconomic calendar will be relatively limited. The main points of focus will be PMI data in Europe and the United States, as well as the May PCE index, a key benchmark for the Fed’s monetary policy decisions.

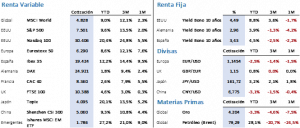

The combination of these factors had a positive effect on equity markets. The S&P 500 gained 0.93% and surpassed 7,500 points by the end of the week. Performance was even stronger in the Nasdaq 100, which rose 2.60%, driven by large technology companies, and closed at 30,406 points. Although U.S. indices did not reach new all-time highs, they came very close to doing so. In Europe, by contrast, new highs were recorded for the second consecutive week. The Euro Stoxx 50 advanced 1.71% to 6,293 points, while the Ibex 35 stood out with a gain of 3.11%, closing at 19,347 points and ending the week very close to its new all-time high.

Fixed income, however, continues to show more erratic behavior. After several sessions of recovery, selling pressure reappeared, pushing yields higher. The 10-year U.S. Treasury ended the week at 4.49%, giving back much of the gains accumulated previously. In Europe, the German Bund saw its yield decline by 2 basis points to 2.98%, while the Spanish 10-year government bond rose to 3.46%. The future evolution of the bond market will continue to depend largely on inflation expectations, which for the time being still fail to provide clearly favorable signals for bond investors.

In commodities, the trend observed during the previous week was repeated. Gold fell 1.55%, affected by rising interest-rate expectations, to $4,172.90 per ounce. Meanwhile, Brent crude declined 7.74% and closed at $80.57 per barrel, although it reached weekly lows of $76.54. The closing price is particularly relevant from both a technical and fundamental perspective. If crude oil were to consolidate below current levels and traffic through the Strait of Hormuz were to return fully to normal, the door could open to further declines toward the $72-per-barrel area. A scenario of greater stability in oil supply would also help reduce inflationary pressures and support greater stability in fixed-income markets.

Finally, the dollar staged a notable recovery following Warsh’s remarks. Against the euro, the exchange rate reached levels of 1.1417 before closing the week at 1.1469, representing a 0.86% appreciation of the U.S. currency. In a scenario of increasing geopolitical and financial stability, one might expect some weakening of the dollar against other currencies. However, the shift in expectations regarding U.S. monetary policy could significantly alter that dynamic in the coming months.

The quote:

And we conclude with the following quote from UN Secretary-General António Guterres, in the week marking the 81st anniversary of the founding of the United Nations: “In a divided world, there is a way forward: dialogue. When we talk, we replace confrontation with cooperation.”

Summary of the performance of major financial assets (06/22/2026)