Financial Markets 30/06/2026

We are approaching the end of the first half of the year, and equity markets have undergone a partial round of profit-taking. The technology sector in general, and particularly the companies most directly linked to artificial intelligence, have experienced the most significant moves. It is noteworthy that this correction has taken place precisely at a time when geopolitical tensions appear to be easing. The most common explanation for this selling once again relates to valuations, which remain demanding, and the substantial infrastructure investment required to support AI development, which could put pressure on future cash flow generation.

The agreement reached between Iran and the United States, on the one hand, and Israel’s commitment not to attack Lebanon, on the other, have allowed Brent crude, as we anticipated last week, to fall back to the USD 72 per barrel area, the level at which it was trading before the conflict in Iran began. As shipping traffic through the Strait of Hormuz gradually returns to normal, supply-side inflationary pressures stemming from the sharp increase in fuel prices should ease over the coming months, provided oil prices stabilize at these levels or continue declining toward the USD 62–65 per barrel range.

Volatility is unlikely to disappear immediately. A solid and lasting framework agreement will be needed for financial assets to reduce the geopolitical risk premium and regain greater stability. One illustration of this volatility can be seen in expectations regarding future Federal Reserve policy moves. Following Kevin Warsh’s remarks after the first meeting he chaired as head of the institution, investors interpreted his tone as considerably more hawkish. Within hours, markets shifted to pricing in two 25-basis-point rate hikes before year-end. However, the subsequent decline in oil prices to levels more consistent with the balance between supply and demand has led investors to reassess those expectations. The current consensus now points to a single rate hike in the latter part of the year, followed by a relatively stable monetary policy throughout 2027.

The week was relatively light in terms of major macroeconomic releases. The most notable data were the preliminary June PMIs, which continued to reflect the strength of the U.S. economy, particularly in the manufacturing sector. In Europe, changes were limited compared with the previous month, with a slight improvement in manufacturing—although it remains in contraction territory—alongside a modest deterioration in the services sector. The most positive surprise came from the revision to U.S. first-quarter GDP, which was increased by half a percentage point to 2.1%. In addition, May PCE inflation came in at 4.1%, in line with expectations, easing concerns about a further acceleration in inflationary pressures. The current week will bring U.S. employment and unemployment figures, as well as the final June PMI readings for both Europe and the United States.

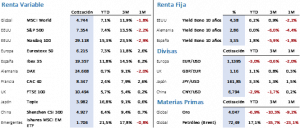

Equity markets ended the week lower as profit-taking in the technology sector weighed on performance; consequently, the greater the technology weighting in an index, the more pronounced the correction. The S&P 500 declined 1.95% to 7,354 points, while the Nasdaq 100 posted a steeper loss of 4.23%, closing at 29,118.24 points. Europe, where large technology companies carry less weight, proved more resilient. The Euro Stoxx 50 fell 1.14% to 6,221.55 points. The strongest performance came from Spain’s Ibex 35, which gained 0.40% to close at 19,347.4 points after reaching a new all-time high of 19,575.30 points.

Fixed income markets reflected a less tense geopolitical backdrop and the sharp correction in commodity prices. The yield on the 10-year U.S. Treasury note fell by 8 basis points over the week to 4.37%. In Europe, declines were even larger: the German 10-year Bund yield dropped by 13 basis points, while the Spanish 10-year government bond yield fell by 12 basis points to 2.85% and 3.34%, respectively. The Spanish bond yield now stands slightly below the midpoint of the range in which it has traded since February 27. Although there is still room for further declines, it appears unlikely that yields will revisit the lows seen at the beginning of 2026.

In commodity markets, Brent crude recorded a correction of nearly 10%. Its close at USD 72.60 per barrel leaves it very close to an important technical support level. Temporary rebounds before resuming the downward trend would not be surprising, but a clear break below USD 72 would open the door to a move toward the USD 62–65 per barrel range. Meanwhile, despite lower bond yields, gold was weighed down by the strength of the U.S. dollar. The U.S. currency reached a new yearly high against the euro, pushing the EUR/USD exchange rate to 1.1325 and exerting pressure across the commodity complex. Against this backdrop, gold declined 3.52%, although it continues to trade well above the previous lows recorded below USD 4,000 per ounce.

The quote:

As we conclude, we would like to express our thoughts and solidarity with the Venezuelan people, devastated by the powerful earthquake that struck last week, with this quote from Arturo Uslar Pietri, one of the most influential intellectual figures in 20th-century Venezuela: “History is nothing but an unceasing beginning again.”

Summary of the performance of the main financial assets (29/6/2026)