Financial Markets 9/9/2025

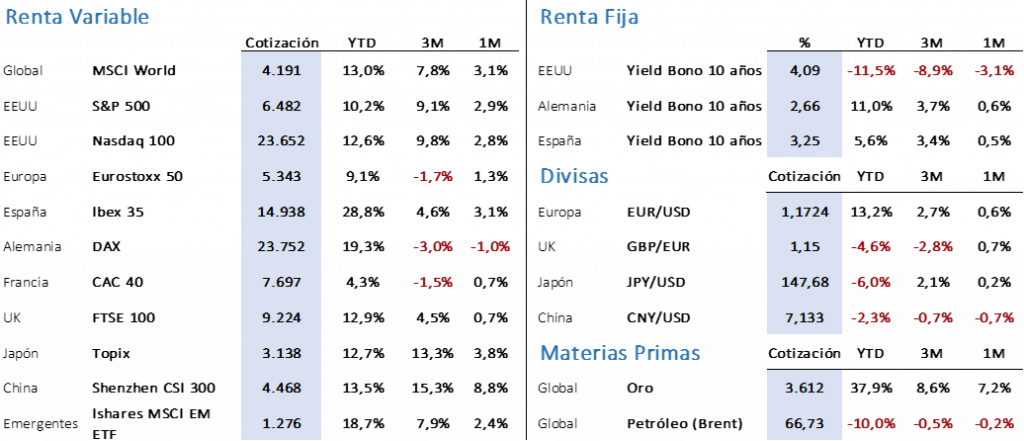

The first week of September saw slight corrections in the main European stock markets, while US stock markets continued to rise, driven by new expectations of interest rate cuts by the Fed. The market is discounting that the Federal Reserve will resume cutting rates as a result of US employment data clearly pointing to a cooling economy for the second consecutive month, but a recession is not being considered in any case. On the other hand, August saw gains of between 2% and 3% in the main indices, which are also very close to their annual highs. The S&P 500 rose 0.32% last week to close at 6,481.50 points after hitting a new all-time high of 6,532.65. The Nasdaq 100 gained 1% to close at 23,652.44 points, despite Nvidia’s significant correction following the presentation of its results. In August, the technology index rose 1.87%.

In Europe, the month began with moderate corrections of -0.57% for the Euro Stoxx 50 and -0.65% for the Ibex 35, after the Euro Stoxx remained flat in August and the Ibex rose 3%. The old continent is being affected by two main factors: on the one hand, the very complicated situation of the French government, which led to a rise in long-term European interest rates (which are being corrected in recent sessions) and which will be subject to a vote of confidence on Monday, September 8; On the other hand, the economy seems to be gaining some traction, which has caused a slight upward movement in short-term interest rates.

In recent weeks, bond markets have reflected the clear difference in expectations between the United States and Europe (FED vs. ECB) regarding what will happen between now and the end of the year. The FED will cut its interest rate two or three times, while in Europe, if there is a final rate cut, it will likely occur in December. As a result, the US yield curve has seen its returns decline, with the 10-year Treasury closing last Friday at 4.09%, down 14 bps from the previous week and 27 bps since the end of July. Meanwhile, movements in Europe have been much smaller, with the Bund falling 6 bps in a week and only 3 bps since July to stand at 2.66%, while the Spanish 10-year bond fell 7 bps and 1 bp respectively, ending with a yield of 3.27%.

As for alternative markets, gold prices have reflected various events, particularly the crisis in the French government and the potential cut in interest rates in the United States. In the last five days, it has risen 3.10% and 8.70% since July, closing at $3,640.12/oz after hitting a new all-time high of $3,653.30. Brent crude has undergone a significant correction, falling to $65.60/bbl, representing a weekly decline of 3.70% and a correction of 9.55% since the end of July. The slower-than-expected growth of the US economy could be a factor in this correction, but in recent days Saudi Arabia has been sending messages to the market about its interest in OPEC+ increasing crude oil production above expected levels.

In terms of macroeconomics, last week saw positive PMI data in Europe, with GDP remaining at +1.5% (estimated 1.4%) and the unemployment rate stable at 6.2%. On the negative side, the CPI rose by one tenth to 2.1% and retail sales fell by -0.5% compared to the expected -0.3%. In the United States, PMIs continue to show the strength of the economy, but labor market data continues to decline, which has served as a catalyst for the debt market. The unemployment rate rose to 4.3% and average hourly earnings rose 3.7% compared to 3.9% previously. For now, wage increases remain higher than inflation.

This week, we will be watching: i) China’s export and import data and the CPI update, ii) in Europe, the ECB meeting, for which no changes are expected, and iii) in the United States, the CPI and PPI data will be released, and on Friday we will see the update of the University of Michigan survey on inflation and consumer confidence.

The Quote:

And we bid farewell with the following quote from Antonio Fraguas Forges, Spanish cartoonist: “Violence is the fear of other people’s ideas and little faith in one’s own.”

Summary of the performance of major financial assets (9/9/2025)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.