Financial Markets 12/11/2025

The beacon of the markets:

The beginning of November brought the first week of significant corrections in the main stock markets, caused by several factors, including: i) the sharp rise in equity prices since the lows of last April, ii) adjusted valuations of many of the companies that have led growth, and iii) doubts among some investors about the hundreds of billions being invested in the development of artificial intelligence.

This does not mean that a bubble scenario is about to burst, as we can say that most experts also agree that the necessary circumstances for a sharp and lasting correction in the stock markets are not in place. Among the aspects being taken into account are: i) not all technology companies depend on AI as their sole growth vector, ii) the balance sheets of leading companies are remarkably healthy, and in some cases they have huge amounts of cash waiting for the opportunity to invest it, iii) profits and margins remain very strong and will continue to do so according to the guidance provided by companies, iv) when there have been corrections of a certain magnitude, valuations have quickly become attractive, a circumstance that has allowed us to see market recoveries in recent years that are even more significant than the falls themselves, v) there appears to be some calm on the geopolitical front, which is helping to generate stability, at least in the short term, and vi) last weekend saw an initial agreement between Democrats and Republicans that will bring an end to the government shutdown in the United States, allowing macroeconomic data to be compiled once again, which serves as a guide for both investors and the FED.

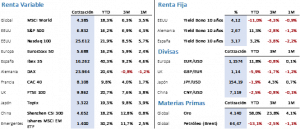

The main stock markets fell last week, but with Europe already closed, the main US indices recovered the significant losses that were occurring mid-session on Friday. In any case, the S&P 500 fell 1.63% to close the week at 6,728.80 points. The Nasdaq 100 fared worse, with the technology benchmark falling 3.09% to close at 25,059.81 points, almost 2% above the day’s lows. In Europe, the Euro Stoxx 50 fell 1.69% and the Ibex 35 fell 0.82%, closing at 5,566.53 and 15,901.40 points, respectively.

Fixed income markets were again trading in a narrow range, but with some volatility in each session. The 10-year US Treasury closed with a yield of 4.09%, 1 bp less than the previous week. In Europe, German and Spanish benchmarks saw long-term debt yields rise by 3 and 4 bps respectively, with the Bund closing at 2.67% and the Bono at 3.18%. Uncertainty over when the Fed will make its next cut and whether the new president will accelerate cuts in 2026 are the factors that could move the markets, which are eager for macro data that could provide clues about the health of the US economy and, in particular, its labour market. In Europe, no changes are expected from the ECB in the coming months.

Brent crude fell 2.21% to close at USD 63.63/bbl, as fears of a significant supply glut continue to weigh on investors. Furthermore, the impact of OPEC+ announcing that it was halting its programme of gradual production increases has so far had a very short-term effect, which could pave the way for a return to the previous trend. In addition, the impact of OPEC+ announcing that it was halting its programme of gradual production increases has had a very short-term effect so far, which could pave the way for further price corrections, especially if the Chinese economy fails to recover. Gold ended the week with a minimal gain of 0.33%, closing at USD 4,009.80/ounce, about 3% above its weekly low. Central banks will continue to support the precious metal, but the change in the geopolitical environment, which is less tense, could trigger further episodes of significant corrections as safe-haven assets become less necessary.

We have entered the final phase of the earnings season. Almost 90% of companies in the S&P 500 have reported their results, and the excellent tone seen from the outset continues. Eighty-three per cent of companies have surprised on the upside with their results, compared to 13% that have disappointed. In addition, average EPS in the third quarter stood at 16.5% compared to the initial estimate of 8.5%, i.e. almost double the estimate, and Nvidia, among others, is yet to report, which it will do on 19 November.

The quote:

And we bid farewell with the following quote from Ralph Waldo Emerson, American writer, philosopher and poet, leader of the Transcendentalism movement in the early 19th century: ‘Believe in yourself; our strength is born of our weakness.’

Summary of the performance of major financial assets (11/11/2025)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.