Financial Markets 18/11/2025

The beacon of the markets:

On Thursday, the US government shutdown came to an end, having become the longest in history after 43 days of inactivity. But as the statistics indicate, the impact on the markets has been negligible, and now they are focusing primarily on understanding two things: i) will the very strong investments being made across the AI sector generate great results in the future or end up causing a sharp fall in the markets? and ii) what will happen to interest rates in the United States? The market seems to be leaning towards stability at the December meeting, as official data on important variables such as employment will not be released until the first few days of December, and October’s data will most likely never be released.

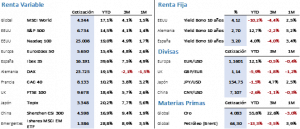

Last week closed with minimal changes on the US stock markets, despite the volatility experienced, especially in Friday’s session, which once again went from less to more. The S&P 500 managed to finish in positive territory at 6,734.11 points (+0.08%), but the Nasdaq 100 did not, as technology stocks are being hit hardest by the spikes in volatility. In any case, the correction was minimal (-0.21%) and it closed above 25,000 points. In Europe, equities had a positive week, recovering what they had lost the previous week. The Euro Stoxx 50 rose 2.33% to close at 5,696.65 points, and the Ibex 35 ended the week with a gain of 2.83%, setting a new all-time high of 16,661.33 points.

Fixed income markets have been the most affected by the change in forecasts regarding the Fed’s upcoming decision at its last meeting of the year. A few weeks ago, the market was betting on a further 25 bp cut, with a probability of over 90%, but at the end of the week that probability was below 45%. In any case, there are still more than three weeks to go before the Fed meets, and the data could alter the forecasts again. The direct consequence was that government bond yields rose by a minimum of 5 bps at the end of the week. The 10-year Treasury ended at 4.15%, while the Bund ended at 2.72% and the Bono at 3.23%. The trend could continue over the next few days, as it will not be until Friday that we have the first relevant data on the US economy that could serve as a guide for the market.

As for alternative markets, precious metals rose, with the sector experiencing a notable upturn in volatility. Gold saw a difference of more than 6% between its weekly high and low, while silver exceeded 12%. At the end of the week, gold was up 2.23%, closing at USD 4,094.20/ounce. Meanwhile, oil is undergoing a continuous change in trend. While on the one hand the consensus is that there is a clear oversupply that will not be corrected in the short term, on the other hand, Ukrainian attacks on Russian oil assets and climate problems in the Gulf of Mexico are affecting production levels. On this occasion, the week ended with a 1.19% rise in the price of Brent to USD 64.39/bbl, a level that continues to contribute to deflation in Europe.

On the macroeconomic front, there was no particularly relevant news from the United States. In China, despite the holiday week, retail consumption grew above forecasts and the unemployment rate corrected by one tenth of a percentage point to stand at 5.1%, but on the negative side, the industrial production index fell to +4.9% from +6.5% previously. Finally, it is worth highlighting the positive GDP data for the third quarter of 2025 in Europe, which rose to 1.4% from the preliminary 1.3%. In addition, investor confidence published by the ZEW institute exceeded forecasts, with September’s industrial production data being the least positive, growing by only 0.2% when the forecast was 0.7%.

For the current week, the most significant events in the United States will be the publication of the minutes of the last Fed meeting and the PMI data. In Europe, we will see the evolution of the CPI and the PMIs, in both cases provisional data for November. The earnings season is in its final phase and can be considered very positive, as US companies are close to doubling their initial earnings per share growth forecasts, pending Nvidia’s announcement on the 19th. To date, 456 S&P 500 companies have reported their results, with average EPS growth of 15.9% (initial estimate +8.5%), of which 83% exceeded estimates and only 13% reported below expectations.

The quote:

We leave you with the following quote from Rabindranath Thakur, poet, philosopher, painter, playwright, musician, novelist and lyricist of the Bengali Renaissance, as well as Nobel Prize winner for Literature: ‘Trees are the earth’s efforts to talk to the listening sky.’

Summary of the performance of major financial assets (17/11/2025)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.