Financial Markets 17/02/2026

We reached the halfway point of February with a week marked by volatility and strong U.S. macroeconomic data. After an initially positive start, with several markets hovering near their all-time highs and others, such as the Euro Stoxx 50, managing to surpass them. Following the sharp drop in precious metals at the end of January, which led to a decrease in appetite for risk assets, the sector now appears to be stabilizing while returning to the fundamental valuation of those assets. As a result, they achieved a slight recovery over the past seven days, although they still remain at a significant distance from their recent highs.

On Wednesday, the market cooled its expectations after the release of employment data that came in far above forecasts, pushing aside (for now) fears of a deterioration in the labor market and, therefore, in consumption. The immediate reaction was a sell-off in equities and a move into fixed income, as the market no longer saw it as necessary for the Federal Reserve to cut interest rates to prevent a slowdown in economic growth. However, on Friday we experienced another unexpected shift, as January inflation data came in below estimates, which were already positive. CPI at 2.4% once again favored fixed income purchases, but this time accompanied by buying in equities. The reason: the key indicators monitored by the Fed are moving in the desired direction (lower inflation and a stable labor market), opening the door for several interest rate cuts in 2026. The data allowed stock markets to rebound from weekly lows, reducing overall declines.

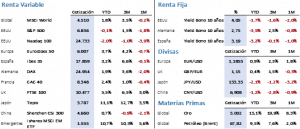

From an equity perspective, Friday’s close confirmed average corrections of around 1.5% across markets. The S&P 500 came within less than 20 points of a new high but ultimately fell 1.39% for the week, closing at 6,836.17 points. The Nasdaq 100 saw its valuation decline by 1.37%, ending at 24,732.73 points. It is noteworthy that despite continued discussion about the significant cumulative declines in software companies over recent months, the index has shown relatively better performance than others. In Europe, the best-performing index was the Euro Stoxx 50, which slipped only 0.21% to close at 5,985.23 points. Meanwhile, the Ibex 35 fell 1.51%, ending at 17,672.40 points. What we are seeing in the markets is a sector rotation that is benefiting a broad range of companies at the expense of the “Magnificent 7” and the themes they lead, particularly software, a sector that is paradoxically being impacted by the development of Artificial Intelligence.

The most significant impact occurred in fixed income, where we saw bond yields decline notably across all markets, driven by the higher probability that central banks will continue easing monetary policy pressure, to a greater or lesser extent depending on the needs of each geographic region. The United States and the United Kingdom will likely lead these cuts, and as a result we saw declines of between 8 and 15 basis points among major 10-year government bonds. The Treasury closed with a yield of 4.06% (-14 bps) and is once again approaching the 4% threshold, a very important short-term reference point for the direction of rates in the United States. In Europe, the Bund closed at 2.76% (-9 bps) and the Spanish 10-year bond at 3.14% (-8 bps). It seems logical that additional declines in European debt yields may be smaller than those in the United States.

As anticipated at the beginning, gold and silver recovered a small portion of the ground lost recently, though not without significant intraday volatility, which in the case of silver exceeded 7% on each trading day of the week. Thus, gold rose 1.33% and closed again above USD 5,000 per ounce, while silver climbed 1.40% to close at USD 78. Meanwhile, Brent crude declined 0.44% to close at USD 67.75 per barrel, and the U.S. dollar also slipped 0.44%, ending the week at 1.1869 against the euro.

The current week will continue to feature macroeconomic references of some relevance, although China will be absent as it celebrates its New Year throughout the week. In Europe, key data releases will include the preliminary February PMIs, the industrial production index, and the eurozone investor confidence index published by the ZEW Institute. Finally, in the United States, attention will focus on industrial production data, durable goods orders, comments from the FOMC minutes, preliminary February PMIs, December PCE data, and the first estimate of GDP growth for the fourth quarter of 2025.

Earnings season continues, with 75% of S&P 500 companies having already reported. As of Friday’s close, 369 earnings reports have been released, showing an average EPS increase of 12.7% compared to the expected 8.8%. So far, 75% of companies have exceeded expectations, while 20% have disappointed.

The phrase:

And we close with the following quote from Henry George, American economist and politician, who gained renown and popularity for his advocacy of a single-tax system based on land: “The law of society is each for all and all for each.”

Summary of the performance of major financial assets (2/16/2026)