Financial Markets 24/02/2026

Last Friday’s close can be considered positive for financial markets, as virtually all asset classes saw their prices rise—albeit for different reasons. This is particularly noteworthy given that the environment has not been one hundred percent favorable. On the geopolitical front, the situation in Iran continues to grow more complex. The U.S. president gave the Iranian government a ten-day deadline to accept his nuclear-related conditions and, to apply pressure, is deploying a significant military contingent to the Strait of Hormuz, near where Russia and Iran are conducting military exercises. Other hurdles investors faced were the Fed minutes, which in their latest meeting conveyed a “wait and see” message given the evolution of the U.S. economy, reinforced by a slightly higher-than-expected PCE reading that remains practically anchored at 3%. In other words, the market has returned to expectations of higher interest rates for longer.

In any case, the most surprising negative data point was fourth-quarter GDP. Compared to the 4.4% growth of the previous quarter, the December close came in at just +1.4%, half of what the market had expected. The main drag on growth was the U.S. administration itself as a result of the government shutdown, which is estimated to have subtracted more than 1.2% from fourth-quarter GDP growth. This is the first preliminary reading and, if confirmed, 2025 GDP would have come in at 2.2%, whereas the market had expected at least 2.5%. In any event, this should be viewed as a temporary impact, as it should not affect the structural growth of the U.S. economy.

The situation in Iran acted as a catalyst for commodity prices. Amid fears of an armed conflict, prices of oil, gold, silver, etc., rose on expectations of supply disruptions in the case of crude, and as safe-haven assets in the case of gold and silver. The move in crude is particularly negative since with prices above USD 70/b, the pace of inflation reduction slows.

On a positive note, we highlight the earnings season. Results remain solid, but investors have shifted their focus from past data to forecasts for the coming quarters. The consequence is that companies that fail to deliver positive surprises are being penalized. Lastly, we learned of the U.S. Supreme Court ruling that declared the global tariffs imposed by Trump illegal, as the law used did not grant the authority applied by the government. In any case, tariff pressure will remain in the short term, as other laws have been enacted that do allow the implementation of tariffs and will at least keep them in place for another 150 days. Moreover, the Supreme Court has not ruled on whether the USD 175 billion collected so far from tariffs must be returned.

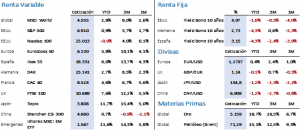

With all this information unfolding throughout the week, stock markets closed broadly higher, with Spain standing out in particular. The S&P 500 rose 1.07% to close at 6,909.51 points, and with very similar performance, the Nasdaq 100 reclaimed the 25,000-point level after gaining 1.13%, which is noteworthy given that noise surrounding software companies still weighs on the tech index. In Europe, gains were somewhat stronger due to the lower weighting of technology stocks and greater participation of financials in the indices. Thus, the Euro Stoxx 50 closed up 1.24%, while the Ibex 35 surged 2.90% to finish at 18,186 points.

In the fixed income market, the 10-year Treasury initially attempted to test the 4% yield level at the beginning of the week, but the Fed minutes did not support the move and it ended with a 3-basis-point increase to close at 4.09%. In Europe, the Bund fell another 2 basis points to 2.74%, while the Spanish 10-year bond saw no changes over the week and ended at 3.14%. Rate cuts in the United States appear set for the second half of the year, while in Germany, improvements in some macroeconomic indicators are easing the pressure generated by the stimulus package aimed at modernizing infrastructure and defense.

Gold edged up slightly to USD 5,080.90/oz, marking its second consecutive weekly close above USD 5,000/oz, where the market appears to be normalizing after the sharp correction experienced during the final days of January and early February. Silver, for its part, rebounded 5.56% to end the week at USD 82.34/oz; however, while gold is just over 10% below its all-time high, silver remains nearly 50% below its peak. Finally, the USD strengthened on expectations of higher interest rates and stood at 1.1782 against the euro, that is, 0.73% lower than the previous week.

On the macroeconomic front, China celebrated its New Year, so there were no reference data. In Europe, PMIs beat forecasts and moved into expansion territory, although industrial production fell 1.4%, and the ZEW investor confidence survey did not reach the expected reading, despite maintaining a positive bias. In the United States, weekly employment data remain positive, as do the Philadelphia Fed manufacturing index and the industrial production index; however, PMIs failed to meet experts’ expectations. For the current week, we do not expect relevant data that could materially affect market performance.

The earnings season is nearing its conclusion, but this Wednesday Nvidia will publish its figures, and analysts will be closely watching both its forward guidance and any investment commitments it may announce. In any case, as of last Friday, 423 companies had reported, of which 75% delivered positive surprises and 20% disappointed. So far, average earnings per share (EPS) have grown 12.9%, compared to the initial forecast of 8.8%.

The quote:

And we close with the following quote from Luís A. Troche Márquez, Bolivian geographic engineer: “The Earth is our refuge; let us help protect and care for it, as the future of many generations depends on it.”

Summary of the performance of major financial assets (23/2/2026)