Financial Markets 10/03/2026

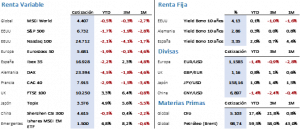

Beacon of the markets: The war in Iran has passed its first week. Iranian resistance appears to be stronger than anticipated by the United States, but the latter confirmed over the weekend that the end of the conflict is near, with the military overthrow of the Iranian regime. In any case, experts expect the attacks could continue for at least another two or three weeks. The impact on financial markets has been limited so far, although there has been a sharp increase in volatility and the price of crude oil. Brent crude has surpassed $100/barrel due to a rise of nearly 30% in the last week and another 30% at the beginning of this week. Regarding returns, stock markets have moved into negative territory, meaning that the profits accumulated since January 1st have evaporated, but the declines from the highs do not yet indicate that a bear market has begun. As for fixed income, price movements have been very intense over the last ten days. Initially, the price increases were very significant due to the search for safe-haven assets, but the secondary effect was not long in coming. The sharp rise in oil prices could lead to further price increases, which would at least delay the anticipated interest rate cuts, and there is even talk of possible rate hikes to counteract the potential inflationary effect. In any case, everything will depend on the duration of the conflict in the Middle East, and in this regard, the market consensus is that the impact will be minimal, with a slight increase in inflation (a few tenths of a percent) and a minimal reduction in global growth forecasts. However, the intensity of the impact will differ between oil-exporting and oil-importing countries. The latter will clearly be worse off, especially the Eurozone countries and Japan. The performance of equity markets last week was the same across all regions. There were widespread declines, but they were more pronounced in those markets that had performed better so far this year. In the United States, the S&P 500 fell 1.90% for the week, closing at 6,734.80 points, or -1.77% year-to-date. The Nasdaq 100 declined 1.27%, closing at 24,643.02 points. The MSCI World dropped 3.28% over the past seven days and entered negative territory for the year (although it is only down 0.53% year-to-date). Europe, meanwhile, suffered more significant declines. The Euro Stoxx 50 fell 5.79%, closing at 5,782.89 points (-0.23% year-to-date), and the Ibex 35 dropped 7%, closing at 17,074.40 points. Europe’s dependence on imported oil and gas has had a significant impact on our financial markets. The fixed-income market has been even more complex to manage, with government bond prices moving nearly 2% in just three sessions (and this trend intensified at the start of the week), causing sharp changes in debt yields within hours. The US Treasury yield rose 17 basis points at Friday’s close, but exceeded 20 basis points during the session before closing at 4.13%. The Bund gained 21 basis points, with its yield settling at 2.86%, and the 10-year Treasury note rebounded 30 basis points, closing with a yield of 3.36%. The US jobs report released on Friday, showing a sharp decline in employment, has added further uncertainty to the market, leading to greater volatility and therefore making it more difficult to set targets. The market faces, on the one hand, fears of a recession due to falling employment and consequently reduced consumption, and on the other, rising inflation that could negatively impact economic growth—again, two simultaneous problems requiring opposing monetary policies to address them. Central banks will likely react by waiting to see what happens before making a decision, and the duration of the war in Iran will be key to this decision. Alternative assets also experienced a particularly volatile week, with silver, for example, seeing a 23% swing between its high and low. The explanation again lay in leverage. When volatility increases, leveraged positions see financial institutions demand higher margin requirements, and if these aren’t met, the positions are closed. This is why downward movements accelerate until leveraged positions are «cleaned up» (the same occurs with short positions during upward movements). In any case, the standout performer was oil. Brent crude rose 28.37% to close at $93.04/bbl on Friday (it reached $119.50/bbl on Monday). If the conflict continues, it could continue to rise, albeit at a slower pace, but it will fall sharply once the attacks end. Gold fell 1.70% to close at $5,158.70/oz, and silver dropped 9.70% to finish the week at $84.31/oz. Finally, the US dollar, like US debt, acted as a safe haven this week. The US currency appreciated against other currencies, closing at 1.1618 against the euro, 1.66% higher than the previous week. On the macroeconomic front, there were significant surprises in several key data points. In Europe, the PMIs exceeded expectations, and the unemployment rate reached 6.1%, a record low. Conversely, the February CPI rose 0.2 percentage points to 1.9% (2.4% at the core level), and retail sales again fell short of expectations, as did the GDP forecast for the fourth quarter of 2025, which came in at 1.2% compared to the previous figure of 1.4% and the initial estimate of 1.3%. In China, the PMIs again remained below 50 and below expectations, but the Caixin survey showed a marked improvement and was in expansionary territory. Finally, in the United States, the PMIs were in line with expectations and in expansionary territory, but retail sales, the unemployment rate, and non-farm payrolls were significantly below forecasts. This last piece of data is the most worrying, as it would again show a potential weakness in the labor market which, if confirmed in the coming months, would jeopardize the economic growth forecasts for 2026. Throughout the week, we will learn the CPI and import and export data in China, the industrial production data for the Eurozone, and in the United States, the January PCE figure along with the February CPI and the Q4 2025 GDP. The quote: And we say goodbye with the following quote from Rodolfo Enrique Cabral Camiña, known by his stage name Facundo Cabral, an Argentine singer-songwriter, poet, and writer: “Blessed is he who knows that sharing a pain is dividing it and sharing a joy is multiplying it.” Summary of the performance of main financial assets (March 9, 2026)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.