Financial Markets 17/03/2026

Beacon of the markets:

The second week of the war in Iran has triggered significant changes in macroeconomic forecasts. The sharp rise in oil prices has increased the likelihood of higher inflation, which in turn has pushed the yield curve upward. Faced with greater uncertainty and higher inflation, investors are demanding higher returns. The general impression is that the armed conflict will last longer than anticipated, and two months of fighting are beginning to be seen as a minimum in terms of duration.

This lack of clarity is causing erratic movements in a range of financial assets. For example, gold is not acting as a safe haven; it is more than 10% below its all-time highs, and selling is occurring. With higher inflation, the probability of interest rate cuts is decreasing, and this had been one of the catalysts for the asset. In any case, we believe that central banks’ gold-buying policies will continue and help to mitigate the severity of corrections compared to other financial products.

The macroeconomic data released in recent days has been overshadowed, and some of it has been quite striking. In China, the CPI clearly rebounded thanks to increased consumption, especially of services directly related to the Lunar New Year holiday. Furthermore, both export and import figures surprised on the upside, more than tripling forecasts and reaching growth rates close to 20%. In Europe, industrial production for January fell by 1.5%, but the December figure was revised upward by almost one percentage point. Finally, in the United States, the CPI confirmed the preliminary figure at 2.4%, while the GDP forecast for the fourth quarter of 2025 was revised downward from 1.4% to a meager 0.7%, but the GDP forecast for the first quarter of 2026 was raised from the previous 2.1% to 2.7%. Furthermore, the PCE figure for January came in at 2.8%, one-tenth of a percentage point below expectations.

Throughout this week, we will see data related to the economic and financial health of the major economic blocs. We highlight the industrial production and unemployment rate figures in China, the ZEW investor confidence index, the final February CPI figure, and the ECB’s monetary policy decision, all in Europe. Meanwhile, in the United States, the industrial production data and the PPI will be released, and the Fed will announce its interest rate decision. These are all important indicators, but they will likely take a backseat to developments in Iran and the Persian Gulf region. The most crucial aspect, however, will be analyzing the central bank statements and how they plan to address the current situation in an environment of extreme volatility and uncertainty.

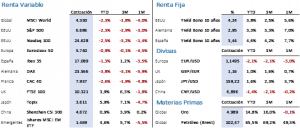

In any case, even though the year-to-date figures are negative, the declines in equity markets were not particularly alarming. In the United States, the S&P 500 fell 1.60% to close at 6,632.19 points, and the Nasdaq 100 dropped 1.06% for the week, ending at 24,380.73 points. In Europe, following the sharp correction of the previous week, stock market movements were more restrained. The Euro Stoxx 50 recovered 0.51% to finish at 5,749.89 points, and the Ibex 35 fell only 0.09% to close at 17,059.30 points.

The fixed-income market, however, is significantly reflecting the uncertainty generated by the sharp rise in crude oil prices. The yields of major bonds rose by more than 10 basis points across the board. The 10-year Treasury rose 16 basis points, with its yield settling at 4.29%. The German Bund saw its yield increase by 12 basis points, closing just shy of 3% at 2.98%, while the Bond, despite being the best performer, climbed 5 basis points to 3.50%.

Commodities once again saw the biggest movements. This week, gold fell 1.88%, closing at $5,061.70/oz, as investors opted to generate liquidity in an asset that has appreciated extraordinarily in the last two years and, due to anticipated inflation, is losing some of its appeal. Brent crude was again the star of the markets, closing above the psychological barrier of $100/bbl and posting a weekly gain of 11.27%, but with rampant volatility. Throughout the week, it reached a low of $81.16/bbl and a high of $119.50/bbl, representing an almost 50% increase from low to high. And if that weren’t enough, the cost of oil was further increased by the USD, which appreciated 1.74% during the week and closed at 1.1416, its lowest level in the last six months. The USD continues to act as a safe-haven asset amid the prevailing uncertainty in the financial markets.

The quote:

And we leave you with the following quote from Edward Bulwer-Lytton, British poet, novelist, playwright, politician, and journalist: “The pen is mightier than the sword.”

Summary of the performance of main financial assets (March 16, 2026)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.