Financial Markets 24/03/2026

Market Insights:

The war in Iran is now in its third week, and the prevailing impression is that it will not end anytime soon. The demonstration of Iranian military capabilities last weekend could put Europe in a complex situation, as it became clear that Iran could attack major European capitals. As the days have passed, investors have lost hope that the conflict will be short-lived, a trend reflected in the price of all financial assets.

On Wednesday, an event occurred that changed the course of the conflict and the forecasts surrounding it. Following Israel’s attack on the Iranian portion of the world’s largest gas field, Iran retaliated by attacking oil assets in the Persian Gulf. Qatar confirmed that the damage to its facilities could affect 20% of its gas production and that it would take several years to recover pre-war production levels. The direct consequence has been a further increase in the price of oil, which has left Brent crude hovering around $112/b at Friday’s close. But more significantly, the spread with West Texas Intermediate has widened to levels not seen since 2014, and even worse, the price of the benchmark barrel in the Persian Gulf has surpassed $150/b. This confirms what we anticipated last week: oil and gas importing countries will fare worse than exporting countries, and there will also be notable differences between those most dependent on raw materials from the Persian Gulf, especially in Asia, and those that import from other regions. Furthermore, exporting countries such as the United States, Canada, Mexico, and Brazil will particularly benefit from the current situation.

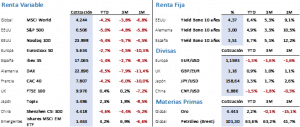

The stock market reaction remains subdued, given the potential impact on the global economy of oil prices above $125/b, but in any case, the S&P 500 has lost 7% from its January highs. Furthermore, the main stock indices closed Friday at the first major technical support level, which corresponds to the highs of last August. Moreover, the markets had been generally rising throughout the week until the attack on Iran’s gas facilities. Last week, the S&P 500 was down 1.90%, closing at 6,506.48 points, while the tech-heavy Nasdaq 100 ended the week at 23,898.15 points, down 1.98%. In Europe, the correction was somewhat greater, especially for the Euro Stoxx 50, which fell 3.90% to close at 5,493.46 points. It is becoming increasingly clear that Europe’s energy dependence is a handicap for its economy. Meanwhile, the Ibex 35 lost 2.02% to close at 16,714 points.

The fixed-income market continues to experience the most unpredictable movements. Bond yields are beginning to reflect an impact on price levels that could lead to a recession. Fears of a sharp increase in prices would be accompanied by an increase in interest rates for two reasons: firstly, to justify returns for investors in the face of higher inflation, and secondly, to restrict the level of financing and slow the economy with the aim of bringing prices down again. Against this backdrop, the yield on 10-year government bonds rose again for the third consecutive week. The Treasury bond climbed 10 basis points to 4.39%, while the Bund rose 6 basis points, surpassing 3% for the first time since October 2013 and reaching levels not seen since 2011. Bonds closed with a yield of 3.58%, 8 basis points higher than the previous week, matching the levels of November 2013.

In alternative markets, Brent crude was once again the star. The spread between the week’s low and high was 20%, highlighting the difficulty of investing in markets with little certainty. Brent closed at $112.19/barrel, representing an 8.77% increase for the week. The other big surprise is the performance of precious metals, which have fallen again for the second week in a row. This can be attributed to investors’ increased need for liquidity, and the fact that gold, in particular, is penalized in an inflationary environment where interest rates are unlikely to decrease and could even rise, thus failing to act as a safe haven asset. Gold dropped 9.62% during the week to close at $4,574.90/oz, more than $1,000 below its high. Finally, the USD has ceased to be a safe haven for investors. Last week it rose 0.88% to close at 1.1517, and it appears that the 1.1415 USD/EUR range is forming a short-term floor.

Macroeconomics remains in the background: we can say that the data as a whole was good, but we continue to see mixed signals. In China, February’s industrial production clearly surprised on the upside, reaching 6.3%, while the unemployment rate rose slightly to 5.3%. In Europe, both inflation and the ECB’s decision unfolded as the markets expected, but the investor confidence index plummeted as a consequence of the war in Iran. In the United States, the employment data was positive, the Fed stuck to its expected script, and while the PPI and Q1 2026 GDP figures were worse than forecast, industrial production and the Philadelphia Fed’s manufacturing index surprised with better-than-expected data. The most important events this week will be the release of the PMI data in both Europe and the United States.

The quote:

And we conclude with the following quote from Andrés Bello López, a Venezuelan jurist, poet, philologist, and diplomat who became a naturalized Chilean citizen and is considered one of the most influential intellectual figures in 19th-century Latin America: “Only the unity of the people and the solidarity of their leaders guarantee the greatness of nations.”

Summary of the performance of major financial assets (March 23, 2026)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.