Financial Markets 07/04/2026

On Monday, April 6, the ultimatum given by the U.S. president for Iran to accept the conditions offered to bring the war to an end expired, and once again, a 48-hour extension has been granted. Apparently, according to several media outlets, they could be close to reaching an agreement for a 45-day ceasefire, which would open the door to negotiating a long-term agreement. So far, all offers have been systematically rejected.

What is clear is that crude oil has settled above 90–100 USD/b, a situation that will generate a notable increase in prices at least in the short term, as we already saw last week with the European inflation data for March. However, after an initial very aggressive reaction, long-term interest rates have corrected toward the upper range of pre-war levels, where government bonds had been trading. On the other hand, both the USD and precious metals seem to have formed a floor, from which a correction to the sharp declines accumulated over more than five weeks since the war began could be starting.

Markets closed last week with significant recoveries even after hitting new lows for the year. In any case, as long as the armed conflict continues, we expect volatility to remain high. Evidence of this is the price of oil, which in the past two weeks has moved more than 20% between its high and low, or bonds, which in just 30 days have seen yields on 10-year benchmarks rise by nearly 60 basis points.

Focusing on macroeconomics, the week delivered a batch of important data that, surprisingly, were good or at least not as negative as the consensus of experts had expected. We highlight job creation in the United States: nonfarm payrolls grew by 178,000 when 65,000 had been expected, a figure partially offset by the upward revision of job losses in February. Retail sales and unemployment rate data were also noteworthy, and to mention a negative figure, services PMIs did not meet expectations and entered contraction territory. In China, March PMI data were released, and both exceeded estimates and stood above 50. Finally, in Europe, CPI grew less than expected in March, with the manufacturing PMI rising more than anticipated. The negative data point was the unemployment rate, which increased by one-tenth to 6.2%.

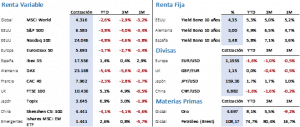

Equity markets closed with widespread gains above 3% despite the fact that nothing has changed in Iran. The war continues, threats remain the order of the day, and the Strait of Hormuz remains closed, which has pushed oil prices 60% above pre-February 27 levels. The S&P 500 rose 3.36% to close at 6,582.69 points. Of note, from the annual high to the low reached last week, the index had corrected by 9.79%. The Nasdaq 100 gained 3.95% to close at 24,045.53 points. Europe did not lag behind this time, with the Euro Stoxx up 3.40%, while the Ibex stood out as one of the best-performing indices, rising 4.48% to close at 17,555.90 points. The first conclusion we can draw from these data is that after the sharp declines and the consequent adjustment in multiples, in the absence of changes in earnings estimates for the current year, investors have taken the opportunity to increase risk in their portfolios.

Debt markets behaved very similarly to equities, with widespread buying driven by very attractive yields unthinkable just a few weeks ago. The 10-year Treasury saw its yield fall by 13 bps to 4.31%, while the Bund declined by 10 bps to close at the 3% threshold, and the Spanish bond fell by 16 bps from 3.64% to 3.48% at week’s end.

Alternative markets performed in line with other assets. The correction in bond yields supported gains in precious metals, with gold rising 3.79% to close at 4,679.70 USD/oz. Brent, despite strong daily volatility, managed to close at 109.03 USD/b, which meant a 3.14% drop from the previous week, but it should not be forgotten that it traded above 119 USD and below 99 USD. As for currencies, the USD appreciated by half a point against the euro to close at 1.1510, but traded nearly two figures higher during the week.

The current week will bring fewer relevant macroeconomic data, which will remain in the background behind news emerging about developments in Iran. In China, March CPI data will be released; in Europe, services PMI and retail sales; and in the United States, the minutes of the last FED meeting, February PCE, and March CPI.

The quote:

We close with the following quote by Audrey Kathleen Ruston, known artistically as Audrey Hepburn, a British actress and model from Hollywood’s golden age: “As you grow older, you will discover that you have two hands, one for helping yourself, the other for helping others”.

Summary of the performance of main financial assets (6/4/2026)