Financial Markets 14/04/2026

The market reaction to the announcement of the 14-day truce agreed by Iran and the United States early last Wednesday was very positive for all financial assets. It remains a short-term truce and tensions are evident, even more so after the failed meeting last weekend in Pakistan where, after more than 20 hours of negotiations, no agreement was reached to make the ceasefire permanent.

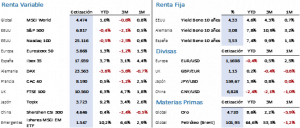

The impact of the ceasefire announcement on stock markets was immediate and strong, to the point that the S&P 500 is once again just 2.7% away from its all-time high. Likewise, the main global stock indices recorded a second week of gains exceeding 3.5%, moving them away from levels considered critical by technical analysts and bringing them closer to their respective historical highs.

In the United States, the S&P 500 rose by 3.56% to 6,816.89 points, while the Nasdaq 100 closed at 25,116.34 points with a gain of 4.45%, despite companies in the software sector remaining under market pressure. In Europe, the Euro Stoxx 50 gained 4.10% to close at 5,926.11 points, and the Ibex 35 came very close to its high, ending the week at 18,204.30 points after rising 3.69% during the period. On an aggregate level, the MSCI World index rose by 3.65% to close at 4,473.96 points.

Greater caution was reflected in the bond market. After more than 6 weeks with oil prices near 100 USD/b, there has been a significant shift in inflation projections and, in turn, in short- and medium-term interest rate expectations. For now, monthly inflation has risen by nearly one percentage point between February and March, at a time when the increase in the price of many goods has not yet fully reflected the higher cost of fuel in sectors such as food, which will also be further impacted by rising costs of many chemical industry products, essential for producing fertilizers and pesticides. In any case, after the initial rise in bond prices following the truce announcement, the initial optimism faded and the weekly change in bond yields did not improve. The Treasury yield fell by 3 bps to 4.32%, while in Europe bond yields rose, with both the Bund and sovereign bonds increasing by 5 and 3 bps to 3.05% and 3.51% respectively.

Lower geopolitical tension and hopes for the end of the war were reflected in lower crude oil prices. Brent fell by 12.68% to end the week at 95.20 USD/b. Precious metals continued their recovery, with gold rising 2.30% to close at 4,787.40 USD/oz, although still 20% below its all-time high. In addition, this greater calm favored a depreciation of the USD, which ended the week at an exchange rate of 1.1720 against the euro.

On the macroeconomic front, in China we highlight the March CPI figure, which stood at 1%, below the expected 1.2% and the previous 1.3%. The higher energy cost was reflected in the PPI, which rose to +0.5% from the previous -0.9%, after many months in negative territory and being one of the key factors behind deflation in China. In Europe, the services PMI fell to 50.2 from 51.9, and retail sales met expectations at -0.2%. Finally, in the United States, employment data were positive, CPI rose less than anticipated, Q4 2025 GDP was revised down again to +0.5%, and both consumer confidence and durable goods orders declined significantly—clear signs that six weeks of war are weighing on business decision-making and consumption dynamics.

Throughout this week, we will learn about relevant indicators in several geographic regions. In China, we will see the unemployment rate, Q1 2026 GDP data, and March export and import figures. Europe will publish the final March CPI data, industrial production figures, and the minutes from the latest ECB meeting. In the United States, we will see PPI data, the Fed’s Beige Book, and the industrial production index.

However, the most relevant development in terms of purely economic information flows will be the start of earnings season, which began yesterday. Over the coming weeks, we will learn about the quarterly results of the world’s largest companies. This week, highlights include Goldman Sachs, JP Morgan, Citi Group, BlackRock, Bank of America, ASML, TSMC, and Netflix. As has been observed since the start of the war, investors appear to have greater confidence in corporate earnings than in aggregate macroeconomic data, which have been significantly affected.

The quote:

We close with the following quote from Stephen Hawking, British theoretical physicist, astrophysicist, cosmologist, and science communicator: “However difficult life may seem, there is always something you can do and succeed at.”

Summary of the performance of main financial assets (13/4/2026)