Financial Markets 28/04/2026

Market Insights:

We are entering the last week of April in a context of relative calm, marked by uncertainty surrounding the resolution of the conflict in Iran. The United States has decided to indefinitely extend the ceasefire initially agreed upon until April 22, under the premise that negotiations were progressing in the right direction. However, since then, no new formal meetings have taken place between the parties with the aim of reaching a definitive agreement. Additionally, late last Saturday, the US delegation canceled its planned trip to Pakistan, a country that had been acting as a regional mediator. This decision stemmed, on the one hand, from the lack of acceptance of some of the proposed conditions and, on the other, from the fact that the announced Iranian delegation did not possess the political standing considered appropriate for high-level negotiations.

This geopolitical environment continues to generate increasingly visible differences between financial assets and regions. US equities have continued to advance and have once again reached all-time highs, supported both by the expectation of a possible end to the conflict and by the release of better-than-expected corporate earnings. In contrast, European stock markets have reflected greater caution in a scenario characterized by persistent inflationary pressures, high interest rates, and, consequently, more moderate growth prospects. This context could lead to downward revisions of earnings forecasts in the coming quarters.

Emerging markets, for their part, showed a more neutral overall performance, although with significant divergences between countries. Commodity exporters performed better than importers, while those markets with a greater weighting in the technology sector were better able to mitigate volatility.

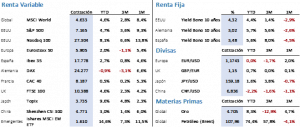

The latest macroeconomic data reinforce this divergent interpretation across regions. In Europe, a clear deterioration in investor sentiment was observed, as reflected in the ZEW Institute survey. Likewise, the services PMI fell sharply and entered contractionary territory, settling at 47.4 points compared to 50.2 the previous month. In the United States, on the other hand, March retail sales, the manufacturing and services PMIs, and home sales all comfortably exceeded expectations, consolidating the positive trend observed in previous months. In equity markets, weekly performance was once again mixed. The S&P 500 rose 0.55% to close at 7,168.08 points, after reaching a new all-time high just three points above the closing level. The Nasdaq 100 stood out, gaining 2.37% to 27,303.67 points, also registering new highs. In Europe, the tone was decidedly more negative: the Euro Stoxx 50 fell 2.69% to close the week at 5,894.73 points, while the Ibex 35 was the worst performer, dropping 4.29% to 17,691.30 points. The MSCI World declined by only 0.38%, closing at 4,632.83 points, although some markets had already finished trading before the final upward move in the United States.

In the sovereign debt market, yields generally rose, but moderately, without reaching levels that could be considered worrisome. Investors continued to emphasize the high level of geopolitical uncertainty: a temporary ceasefire, with no clear progress toward a short-term resolution. As long as the Strait of Hormuz remains closed, oil prices will continue to hover above theoretical levels, further bolstering inflation expectations and, consequently, forecasts regarding central bank action. In this context, the market is pricing in two additional 25-basis-point rate hikes by the ECB, while anticipating no action from the Federal Reserve for the remainder of the year. As a result, the yield on the 10-year US Treasury note rose by 7 basis points to 4.31%, the German Bund climbed 4 basis points to 3.01%, and the Spanish bond saw its yield increase by 6 basis points to 3.45%. In commodity markets, the optimism of the previous week gave way to a more cautious stance. Brent crude continued its upward trend throughout the week amid a lack of geopolitical developments, as a lack of information typically translates into increased uncertainty and more defensive strategies. The European benchmark crude rose 16.54% during the week, closing at $105.33 per barrel. With rising oil prices and rising interest rates, precious metals saw selling, with gold falling 1.83% to $4,790.40 per ounce. Meanwhile, the US dollar appreciated slightly against the euro, closing at $1.1722 per euro.

Several key macroeconomic data will be released this week. China will release its PMIs. In Europe, the ECB will meet and is expected to keep interest rates unchanged. The unemployment rate, GDP for the first quarter of 2026, and the April CPI will also be released. In the United States, the March PCE, April PMIs, and first-quarter GDP will be published, and the Federal Reserve will maintain interest rates at its FOMC meeting, chaired for the last time by Jerome Powell. As for the earnings season, the main driver of the US stock market, it continues to evolve very positively. As of Friday’s close, 28% of the companies comprising the S&P 500 had already reported their results, and of those, 84% exceeded analysts’ expectations. Average earnings per share growth stands at 15.1%, which would allow for a sixth consecutive quarter of double-digit corporate profit growth.

The quote:

And we leave you with this quote from John Roy Major, British Conservative Party politician and Prime Minister of the United Kingdom from November 28, 1990, to May 2, 1997: “Recovery begins from the darkest hour.”

Summary of the performance of major financial assets (April 27, 2026)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.