Financial Markets 12/05/2026

One more week, equity markets maintained a clearly constructive tone and once again reached new all-time highs, supported by an especially strong quarterly earnings season. U.S. equities once again led the gains, followed by the rest of the global markets, albeit with more moderate advances, with isolated exceptions such as the Korean market, where the heavy weighting of the technology sector boosted relative performance.

On the geopolitical front, the situation in Iran remains apparently stable thanks to the truce currently in place, although this balance continues to be fragile. The increasingly harsh rhetoric in negotiations, together with ongoing threats, keeps alive the risk of a sudden deterioration in the scenario. As we have pointed out in recent weeks, this tension is reflected more clearly in fixed income and commodity markets, which continue to act as the main indicator of geopolitical risk and its potential macroeconomic implications.

While the market remains attentive to a possible definitive ceasefire in the Middle East, economic activity continues its course and the macroeconomic and corporate calendar moves forward normally. Overall, the week’s balance was once again positive. In China, export and import data showed very significant growth, clearly above double digits, suggesting that the economy continues to display strong momentum, although part of this behavior could be explained by an acceleration of trade operations ahead of a potentially more complex environment. In Europe, although the services PMI remained in contraction territory, both the manufacturing PMI and retail sales exceeded forecasts. In the United States, the published data continue to confirm the strength of the economy, with no major negative surprises. Particularly noteworthy was the labor market, with the creation of 115,000 jobs in April, well above the expected 65,000. Added to this were stronger-than-expected industrial activity and constructive signals in the residential housing market.

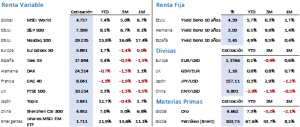

The technology sector continues to be the main driver of equity market gains. Last week, the Nasdaq 100 advanced 5.50% to 29,234.99 points, marking a new all-time high and accumulating a 16% gain so far this year. Meanwhile, the S&P 500 rose 2.34% to 7,398.93 points, closing very close to new highs. In Europe, gains were more contained, both due to the lower weighting of the technology sector in the indices and the greater fear of a more pronounced economic impact stemming from the geopolitical conflict. The Euro Stoxx 50 advanced 1.55% to 5,972.65 points, while the Ibex 35 rose 0.61% to 17,889.40 points. Globally, the MSCI World closed at 4,757.30 points, just 10 points below its all-time high, with a weekly gain of 1.78%.

In the fixed income market, the week ended with limited movements in yields, although with a wide fluctuation range during the previous days, reflecting persistent uncertainty. The duration of the conflict and its final impact on inflation and growth remain the key unknowns. The yield on the 10-year U.S. Treasury bond fell by 2 basis points, the German Bund by 3 basis points, and the Spanish government bond by 8 basis points, standing at 4.36%, 3.00%, and 3.42%, respectively. Even so, these levels remain between 35 and 40 basis points above those recorded before the beginning of the conflict.

The slight correction in interest rates favored the performance of precious metals. Gold rose 1.86% to USD 4,730.70/ounce, also supported by the depreciation of the dollar, which weakened by 0.55% against the euro. The most volatile asset was once again oil. Brent traded again within a range exceeding 10% and ended the week down 6.36%, which could be interpreted as a signal of expectations for a possible short-term agreement.

Looking ahead to the current week, the macroeconomic calendar will be somewhat less demanding, although still with relevant references. In China, CPI data will be published, with no significant changes in trend expected. In Europe, the investor confidence index published by the ZEW institute, industrial production data, and the revision of first-quarter 2026 GDP will be released. In the United States, attention will focus on CPI, retail sales, and industrial production.

On the corporate front, earnings season is entering its final stretch. To date, 89% of S&P 500 companies have reported earnings, with 84% of them beating analysts’ expectations. Average earnings-per-share growth stands at 27.7%, compared to the 13.1% estimated at the start of the reporting season. While the energy sector has made a relevant contribution, the technology sector has once again been the main driver. Finally, earnings forecasts have been revised upward: by 2.1% for the next quarter and by 3.4% for the full year. Despite the geopolitical backdrop, market consensus continues to anticipate that 2026 will be an especially favorable year for listed companies.

The quote:

And we say goodbye with the following quote from David Frederick Attenborough, British scientist and natural history broadcaster: “Anyone who believes that infinite growth can exist in a finite environment is either a madman or an economist.”

Summary of the performance of major financial assets (11/5/2026)