Financial Markets 19/05/2026

Market Insights:

The truce in the Middle East holds, although the situation is progressively deteriorating due to the lack of progress in negotiations. The latest statements from the parties involved show a growing divide, with demands increasingly distant from any potential agreement. In this context, the price of oil remains above $100 per barrel, while inflation continues to rise globally.

Last Friday, debt markets saw a widespread increase in yields across the entire yield curve. In the United States, yields rose by more than 3%, reaching levels not seen since February 2015. In Europe, the German Bund closed at its highest level since the start of the conflict in Iran. Inflationary pressure stemming from rising commodity prices has persisted for the past twelve weeks, intensifying recently after the release of a higher-than-expected US CPI. Inflation currently stands at 3.8%, almost double the Federal Reserve’s target. This data has triggered a significant shift in market expectations: investors have gone from anticipating rate cuts just two months ago to pricing in a possible rate hike in 2026, when the previous week monetary policy stability was assumed.

The rise in interest rates weighed on equity performance on Friday, erasing the gains accumulated during the week. Key indices such as the Nasdaq 100 interrupted a six-week winning streak, while the S&P 500 managed to close marginally positive. In Europe, the impact was more pronounced, reflecting greater economic vulnerability to tensions in the Strait of Hormuz. Furthermore, the geopolitical context continues to deteriorate, with pro-Iranian militias intensifying their attacks in the region, increasing the risk of escalating conflict.

Despite this environment, macroeconomic data continues to show resilience, particularly in the United States. In China, the April CPI came in at 1.2%, slightly above expectations, with even stronger growth in the PPI. In Europe, economic weakness was confirmed, with GDP growth of 0.8% in the first quarter of 2026. In the United States, beyond the inflation figure, retail sales showed moderate growth, while the second-quarter GDP estimate (4%) and leading indicators—weekly employment, industrial production, and the Empire State Manufacturing Index—surprised positively.

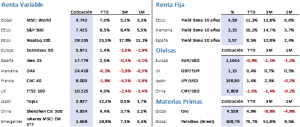

On a weekly basis, equities closed with a negative balance, influenced by Friday’s declines. The S&P 500 advanced slightly by 0.13% to 7,408.50 points, after having reached a new all-time high of 7,517.12 points during the week. The Nasdaq 100 fell 0.38% to 29,125.20 points, but reached a new high during the week. In Europe, the Euro Stoxx 50 dropped 1.41% and the Ibex 35 fell 1.49%, reflecting the region’s greater sensitivity to the macroeconomic environment. Meanwhile, the MSCI World index declined 0.33%.

Fixed-income markets were the hardest hit, especially on Friday, with a significant increase in borrowing costs. The yield on the 10-year US Treasury rose 24 basis points to 4.60%. In Germany, the Bund climbed 15 basis points to 3.15%, its highest level of the year. In Spain, the 10-year bond rose 18 basis points to 3.61%, near its highest level of the year. In commodities, performance was mixed. Gold fell 3.57% due to rising real interest rates and a stronger dollar. Silver saw a sharper decline, dropping nearly 15% and reversing the strong gains of the previous week. Oil continues to be the main focus of attention, with high weekly volatility. This week, Brent crude rose 7.87% to $109.26, amid disruptions to shipping in the Strait of Hormuz. Meanwhile, rising US yields and expectations of monetary tightening boosted the dollar, which appreciated 1.36% against the euro, reaching 1.1626.

Looking ahead to the week, attention will be focused on several key macroeconomic indicators to assess the impact of the conflict on the global economy. Industrial production and unemployment data will be released in China. In Europe, the final April CPI and preliminary May PMIs will be released. In the United States, the minutes from the last Federal Reserve meeting, the Philadelphia Manufacturing Index, and the leading PMIs will be published.

Finally, the earnings season is entering its final phase. To date, 89% of companies have reported results, of which 84% have exceeded estimates. Average EPS growth stands at 27.7%, significantly above the expected 13.1%, which continues to be the main support for market performance.

The quote:

And we conclude with the following quote from Gustav Mahler, the Austro-Bohemian composer and conductor whose works, along with those of Richard Strauss, are considered the most important of the post-Romantic period: “Tradition is not the worship of ashes, but the preservation of the fire.”

Summary of the performance of major financial assets (May 18, 2026)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.