Financial Markets 02/06/2026

Positive market reaction resumed following last Thursday’s announcement, in which Iran and the United States communicated a preliminary agreement to establish a 60-day negotiation period. This framework would allow progress on key issues such as Iran’s nuclear program, the opening of the Strait of Hormuz, and the release of frozen funds. However, the agreement has not yet been ratified by either government, adding a further element of uncertainty to the already heightened tensions in the Middle East (indeed, on Monday afternoon Iran announced that it was suspending negotiations with the United States until Israel halts its offensive in Lebanon).

The mere announcement triggered significant movements across financial markets at the end of last week, with a broad impact on different asset classes. Particularly noteworthy was the decline in fixed-income yields, reflecting expectations that a potential agreement could help contain inflationary pressures without leading to an economic recession. At the same time, oil prices posted a significant correction on the prospect of a move toward ending the conflict. Brent crude fell nearly 10% in two sessions, declining by around USD 10 per barrel and settling near USD 90.

Beyond geopolitical developments, the global economy continues to perform well, albeit with uneven dynamics across regions. China continues to show relative stability, although within a flat growth environment that does not yet allow for clear trend identification. In the United States, first- and second-quarter GDP data came in below expectations, although other indicators—such as the Chicago PMI and durable goods orders—surprised positively. Likewise, the latest surveys point to a slight improvement in consumer confidence.

In Europe, amid a lack of major macroeconomic releases, attention has focused on the minutes of the ECB’s latest meeting. The institution maintains a cautious stance focused on controlling inflationary pressures while assessing potential structural risks. Although the decision to keep the deposit facility rate at 2% was unanimous, a more hawkish bias is evident regarding interest-rate expectations, to the extent that some members reportedly did not rule out a rate hike at the April meeting. Rising energy costs could generate second-round effects and extend the period during which inflation remains above the 2% target. At the same time, growth in the euro area is being affected by moderating consumption and investment. In this context, the ECB will continue to monitor macroeconomic variables closely, although, given current developments, the market is pricing in further rate hikes throughout 2026, the number of which will depend largely on the evolution of the conflict and the normalization of energy markets.

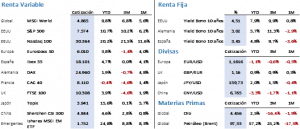

Equity markets posted broad gains, once again led by the technology sector, despite Nvidia remaining approximately 10% below its highs. The week progressed relatively calmly until Thursday’s announcement, after which capital inflows into risk assets intensified. The S&P 500 closed up 1.43% at 7,580.06 points. The Nasdaq 100 advanced 2.89% to 30,333.18 points, reaching new all-time highs, as did the S&P 500 and the MSCI World. In Europe, the Euro Stoxx 50 recorded the most modest increase, rising 0.52% to 6,050.54 points, while the Ibex 35 gained 2.10% to 18,362.90 points, finishing very close to its highs.

Fixed-income markets also reflected the new environment, with yields falling by more than 10 basis points: 10 bps for the Bund, 11 bps for the Spanish government bond, and 12 bps for the U.S. Treasury. Yields ended at 2.93%, 3.36%, and 4.45%, respectively, approaching the midpoint of the range observed since the beginning of the conflict.

In commodities, movements were consistent with the shift in expectations that emerged on Thursday. Until then, oil had been trading within a narrow range, while precious metals were experiencing slight corrections due to movements in real rates and inflation expectations. Following the announcement, Brent crude fell 11.10%, closing at USD 92.05 per barrel after briefly breaking below the USD 90 level. Precious metals, meanwhile, reversed their initial losses: gold rose 1.19% to USD 4,593 per ounce, although it remains 20% below its annual highs. The U.S. dollar depreciated by 0.50% against the euro, anticipating a scenario of greater geopolitical stability.

As is customary at the beginning of the month, the current week will be marked by the release of key macroeconomic data, with particular attention on PMI figures and employment data. Markets will analyze these indicators closely for signs confirming the resilience of the economic cycle or, conversely, pointing to a medium-term slowdown, particularly in the United States.

Quote of the Week:

We conclude with the following quote from Robert Francis Prevost, the 267th Pope of the Catholic Church and the ninth Sovereign of Vatican City, on one of today’s most widely debated topics: “Technology can heal, connect, educate, and care for our common home; but it can also divide, exclude, and generate new injustices.”

Summary of the performance of major financial assets (06/01/2026)