Financial Markets 09/06/2026

Last Sunday marked the first 100 days of the war in Iran. Since the ceasefire was announced on April 8, the situation in the region has remained extremely tense, with “controlled” attacks by both sides and flimsy excuses used to justify each new offensive. Against this complex geopolitical backdrop, what does seem evident is the growing decoupling between the evolution of the conflict in the Middle East and the behavior of financial markets.

The war continues to exert upward pressure on both commodity prices and global inflation expectations. However, risk assets, especially equities, had maintained a clearly bullish trend thanks to the strong corporate earnings reported for the first quarter of the year. Furthermore, these figures were accompanied by upward revisions to full-year forecasts, coming in well above the market’s initial estimates. Nevertheless, every major rally eventually comes to an end, and last Friday marked the long-anticipated turning point. The S&P 500 suffered a significant correction, ending a streak of nine consecutive weeks of gains. Most strikingly, the decline was triggered by the release of extraordinarily strong employment data in the United States.

Nonfarm payrolls reached 172,000 compared to the 85,000 expected by consensus. In addition, the previous reading was revised upward from 115,000 to 179,000. This strength in the U.S. labor market quickly spilled over into the bond market, driving a sharp increase in bond yields, further reinforced by rising inflation expectations and the prospect of higher interest rates for longer. As a result, selling pressure intensified throughout the session, leading to particularly negative market closes.

Adding to this environment were, once again, comments from President Trump, who has continued to inject volatility into the markets on an almost daily basis since the conflict began. Statements such as “the war is about to end” or “Iran is eager to sign a peace agreement, but they are afraid to say so” once again generated uncertainty among investors. Moreover, the president reignited the debate over tariffs on China, further damaging market sentiment and accelerating the sell-off during Friday’s session.

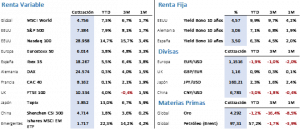

This combination of factors ultimately created the perfect environment for a swift round of profit-taking after the strong gains accumulated over just two months. The S&P 500 ended the week down 2.59%, closing at 7,383.74 points. The technology sector was among the hardest hit: the Nasdaq 100 fell 4.53% over the week, closing at 29,857.60 points, and at one point accumulated losses of nearly 6% during Friday alone. It is particularly noteworthy that both indices had reached new all-time highs only a few sessions before the correction occurred, reflecting the strength previously displayed by the U.S. market.

In Europe, the move was considerably more moderate. First, because the gains accumulated were significantly smaller than those on Wall Street. Second, because European macroeconomic data continue to show no excessive strength capable of materially increasing interest rate expectations. And finally, because much of the decline in the United States occurred after European markets had already closed. As a result, the Euro Stoxx 50 managed to finish the week with a slight gain of 0.19%, reaching 6,062.07 points, while the Ibex 35 slipped a modest 0.10%, ending at 18,344.90 points.

In fixed income markets, yields reacted with broad-based increases of around 10 basis points. The U.S. 10-year Treasury ended the week at 4.54%, nine basis points above the previous close. In Europe, the German Bund and the Spanish government bond rose by 11 and 12 basis points respectively, reaching 3.04% and 3.48%, thereby erasing much of the gains achieved the previous week.

In commodity markets, new expectations regarding U.S. interest rates triggered notable declines. Gold fell 4.96% over the week to USD 4,365.30 per ounce, while silver posted even steeper losses. Meanwhile, Brent crude oil, which had risen sharply during the week amid the lack of definitive progress regarding the reopening of the Strait of Hormuz, corrected on Friday and ultimately ended the week up a moderate 1.09%, closing at USD 93.09 per barrel. Another beneficiary was the U.S. dollar, which appreciated against major currencies. Against the euro, the exchange rate closed at 1.1521, representing a weekly gain of 1.19% for the U.S. currency.

From a macroeconomic perspective, beyond the U.S. employment figures, the week delivered relatively positive signals. In China, the private Caixin PMI surveys came in slightly above expectations. In Europe, PMIs also exceeded consensus forecasts, although the services sector, with a reading of 47.2 points, remains in contraction territory. In addition, retail sales disappointed, the unemployment rate was revised up by one-tenth to 6.3%, and first-quarter GDP growth was revised down from the initial 0.8% to a weak +0.3%. In the United States, most indicators maintained the positive tone reflected in the labor market. PMIs, JOLTS, ADP employment figures, and the unemployment rate came in line with or above expectations. The only negative note came from the Atlanta Fed GDPNow estimate, whose forecast for second-quarter growth was reduced from 3.8% to 3.0%.

Looking ahead to this week, market attention will focus on foreign trade figures and, especially, the release of China’s CPI data. In Europe, the main focus will be the ECB meeting, where consensus expects a 25-basis-point rate hike, from 2.0% to 2.25%. Meanwhile, in the United States, the University of Michigan surveys on inflation expectations and consumer confidence will also be key.

Quote:

We conclude with the following quote from Pope Pius XI, on the occasion of the ratification of the founding of Vatican City, commemorated on June 7: “The Vatican City State is a small reality, but one with an immense soul.”

Summary of the performance of major financial assets (06/07/2026)