Financial Markets 07/07/2026

Market Insights:

After the previous week’s declines, and despite it being a semi-holiday week in the United States, stock markets recovered some of their lost ground. The macroeconomic data released contained both positive and negative surprises, although overall, they supported the upward trend in equities. The geopolitical front had less of an impact than in previous weeks, despite Iran’s refusal to meet with US envoys in Qatar at the beginning of the week. This relative calm allowed the price of crude oil to remain close to the previous week’s closing levels, a factor that contributed to the positive performance of the markets and, in the case of Europe, allowed several of its main indices to reach new all-time highs.

The macroeconomic data released showed that in China, everything remains practically the same: no major developments, but also no particularly worrying signs, beyond the problems in its real estate sector and weak domestic demand. The PMIs were slightly above 50 points, although without any significant improvement. In Europe, the PMIs also modestly exceeded expectations, the unemployment rate fell again to 6.2%, and, most importantly, the preliminary June CPI data surprised on the upside. Headline inflation moderated to 2.8% from the previous 3.2%, below both the market consensus of 3% and the previous figure. Meanwhile, core inflation declined to 2.4%, just two-tenths of a percentage point away from its lowest level in the last five years.

This week, the United States accounted for the largest number of negative surprises. The manufacturing PMI fell by more than one point when the market had expected an improvement in the June reading, and the Atlanta Fed’s GDP estimate for the second quarter of 2026 plummeted to a mere 1.2%. However, as is typical at the beginning of each month, attention was focused on the labor market. The week began strongly thanks to the JOLTS survey, which showed 7.6 million job openings, about 300,000 more than expected. However, both the ADP employment survey and non-farm payrolls surprised with figures significantly lower than estimates. The most significant figure was the one released on Thursday: only 57,000 jobs were created compared to the 114,000 expected by market consensus. Furthermore, the May figure was revised downward, from 172,000 to 129,000 jobs. This situation should help moderate expectations regarding the strength of the labor market and, therefore, give the Fed more leeway to avoid premature intervention.

The current week will be very quiet in macroeconomic terms. China will release its June CPI data. In Europe, the minutes from the last ECB meeting and retail sales figures will be published. In the United States, the services PMI and the minutes from the Federal Reserve’s Monetary Policy Committee meeting will be released.

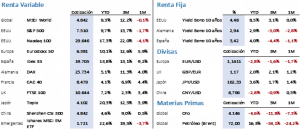

In equities, gains were widespread across global stock markets, despite significant corrections in some technology subsectors, such as microprocessors, and in large-cap companies like Tesla, which fell 7.5% during the week. In the United States, the S&P 500 advanced 1.75%, closing at 7,483.24 points, while the Nasdaq 100 managed to finish in positive territory with a 0.72% gain, reaching 29,329.21 points. In Europe, both the Euro Stoxx 50 and the Ibex 35 reached new all-time highs, very close to their weekly closing levels, settling at 6,412.68 and 19,852.40 points, respectively, with gains of 3.07% and 2.20%.

Government bonds saw their yields rise. The strong job vacancy data led the market to believe that a US interest rate hike could be considered a given, and even anticipated before the July meeting. The yield on the 10-year US Treasury rose 12 basis points to 4.49%, while in Europe, the German Bund and the Spanish Bond rose 8 basis points, closing at 2.93% and 3.42%, respectively. The Treasury rebounded from the lows marked in May, while the Bund and the Spanish Bond did so from levels not seen since the first ten days of March, both remaining less than 25 basis points from the lows of the year. Precious metals advanced despite rising interest rates. Gold appreciated 2.22%, closing at $4,187.3 per ounce. Brent crude, meanwhile, rose slightly by 0.18%, remaining very stable in the $71-$72 per barrel range. A break below this level could open the door to further declines of 10% or even more, which could occur as the Strait of Hormuz returns to normal and resumes the transit of more than 100 ships per day, compared to the just over 30 that have passed through in recent days. Furthermore, the US dollar weakened against the euro, with the exchange rate settling at 1.1437, representing a weekly depreciation of 0.46%.

The quote:

And we conclude with the following quote from Maria Salomea Skłodowska-Curie, better known as Marie Curie, a pioneer in the field of radioactivity and the first and only person to receive two Nobel Prizes in different scientific disciplines, Physics and Chemistry: «We cannot hope to build a better world without improving individuals. To do this, each person must strive to be a better person and, at the same time, share a general responsibility for humanity as a whole.»

Summary of the performance of major financial assets (July 6, 2026)

This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the individuals who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without prior notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation, or solicitation to purchase or subscribe to securities or other instruments, or to make or cancel investments, nor may it serve as the basis for any contract, commitment, or decision of any kind.

The information included in this report has been obtained from public sources considered reliable, and although reasonable care has been taken to ensure that the information included in this document is neither uncertain nor ambiguous at the time of publication, we do not represent that it is accurate or complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any direct or indirect loss that may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcomes.