Challenging Financial Logic: The Risks of Putting a Price on Natural Life with Biodiversity Credits

23.04.24

The topic of the week:

The use of biodiversity credits as a financial tool has emerged as a seemingly innovative response to the global crisis of biodiversity loss. However, behind this apparent solution lies a series of risks and ethical dilemmas that deserve deep reflection.

Biodiversity credits, like carbon credits, are presented as a way to offset environmental damage caused by human activities, allowing companies to «compensate» for the destruction of biodiversity by investing in conservation projects. At first glance, this idea may sound promising: why not use the power of the market to protect nature? However, this simplistic perspective ignores a number of inherent risks in this approach.

First, there is the problem of assigning a monetary value to wildlife and natural ecosystems. How can we calculate the «price» of an endangered species or a unique habitat? In doing so, we run the risk of trivializing the intrinsic importance of biodiversity and reducing it to a mere commodity in the financial market. Is the life of one particular species worth more than another?

Furthermore, there is a danger that biodiversity credits could foster a «compensation» mentality that allows companies to continue destructive practices under the illusion that they are «offsetting» their negative impacts. This could lead to false complacency and a reduction in real efforts to address the underlying causes of biodiversity loss, such as deforestation, urbanization, and pollution.

Biodiversity credits also pose practical challenges, such as the difficulty of measuring and monitoring the real benefits for biodiversity of conservation projects. Without rigorous oversight and proper evaluation, there is a risk that these projects will not achieve their stated goals and will not provide the expected benefits for nature. The recent rise in the popularity of biodiversity credits has also raised concerns about their potential to become a form of «greenwashing,» allowing companies to improve their environmental image without actually addressing the negative impacts of their activities.

Ultimately, we must recognize that biodiversity is a fundamental element of life on Earth and that its protection cannot be reduced to simple financial transactions. Instead of relying on simplistic market-based solutions, we need to adopt a more holistic approach that recognizes the intrinsic value of nature and promotes active conservation and restoration of ecosystems.

In a world where biodiversity loss continues at an alarming rate, we must face the challenge of protecting wildlife and natural ecosystems with the seriousness and urgency they deserve. This will require a fundamental change in our relationship with nature, moving away from a mentality of exploitation and towards one of respect and care

Spotlight on Markets:

The conflict in the Middle East has been the main catalyst for the poor performance of the markets in recent days. All this without ignoring the tension generated by macroeconomic data and its impact on the comments of central bank officials, and also taking into account that we are in the midst of earnings season, which will help to provide a clearer perspective on how the current year may unfold at the business level.

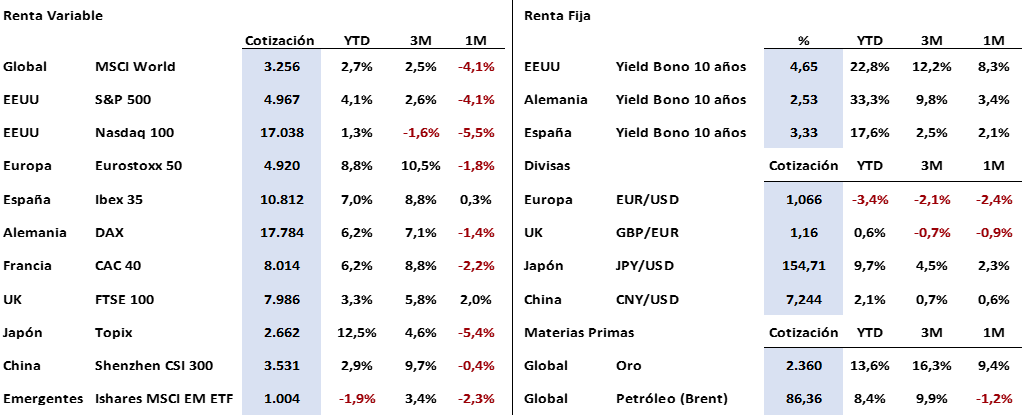

The main casualty of this combination of factors has been equities, and for the third consecutive week we have seen corrections in the major indices. Thus, the S&P 500 fell more than -3%, the Nasdaq 100 corrected -5.36% and the Eurostoxx 50 fell only -0.75%. The discrepancy with the general trend was the Ibex 35, which rose last week by +0.41% despite the volatility that could be seen in all sessions.

The fear that the conflict between Israel and Palestine could escalate with strong Iranian participation in the conflict also caused sales in fixed income assets, so the benchmark ten-year bonds of the US, Germany and Spain saw their yields rise 10, 14 and 12 basis points, respectively, to leave returns at levels of +4.62%, +2.50% and +3.32%. These are levels that could attract the interest of more conservative investors again.

The situation changed slightly throughout the week, and the idea of a much stronger economy than previously estimated became consolidated. Analysts are beginning to seriously consider the possibility that the FED will not carry out more than two interest rate cuts of 25 basis points in 2024, and it is not even ruled out that there could be fewer or that they could even be forced to raise interest rates again. On the part of the ECB, the prevailing idea is that it will carry out its first move in June to end the year with up to four interest rate cuts (the final number will be conditioned by what the FED does).

Regarding the US, it is worth noting again that the main known macroeconomic data exceeded expectations (a factor that is hindering the FED’s possibilities of relaxing its monetary policy), we highlight the Philadelphia Fed manufacturing index, +15.5 points compared to an estimate of +1.5, the Atlanta Fed raised its forecast for 2024 GDP by one tenth to +2.9%, or retail sales which rose by +0.7% in

March compared to a forecast of +0.4%. The discordant note was struck by the real estate sector, whose housing starts data corrected by -14.7% when a minimum slowdown of -2.4% was expected. In Europe, the CPI figure remained at the +2.4% estimated by the market, and for the first time in a long time, China surprised with a GDP growth of +5.3% when +4.8% was expected.

For the current week, we should pay attention in Europe to the data from the services and manufacturing PMIs. In the US, there will be several important references such as the preliminary GDP for the first quarter, the PCE for March (the FED’s favorite indicator to interpret how inflation will evolve), for which a minimum increase to +2.6% is expected (+2.5% previously), durable goods orders, the manufacturing PMI, or the University of Michigan’s estimates for inflation and consumer confidence.

We say goodbye with the following quote from Jacques Yves Cousteau, a marine researcher and biologist who studied the sea and its inhabitants: «Future generations will not forgive us for wasting their last chance, and their last chance is today.»

Resumen del comportamiento de principales activos financieros (22/4/2024)

Please note: This report does not provide personalized financial advice. It has been prepared independently of the specific financial circumstances and objectives of the people who receive it.

This document has been prepared by Portocolom Agencia de Valores S.A. for the purpose of providing general information as of the date of issuance of the report and is subject to change without notice. Portocolom Agencia de Valores S.A. assumes no obligation to communicate such changes or to update the content of this document. Neither this document nor its content constitutes an offer, invitation or solicitation to purchase or subscribe for securities or other instruments or to make or cancel investments, nor may it serve as the basis for any contract, commitment or decision of any kind.

The information contained in this report has been obtained from public sources and considered reliable. Although reasonable care has been taken to ensure that the information contained in this document is not inaccurate or misleading at the time of publication, we do not represent that it is accurate and complete and it should not be relied upon as such. Portocolom Agencia de Valores S.A. assumes no responsibility for any loss, direct or indirect, which may result from the use of the information provided in this report. Past performance of variables may not be a good indicator of their future outcome.